How to organize finances in an easy way

Erin Bruehl

|

October 6, 2021

Erin Bruehl

|

October 6, 2021

It's easy enough to think of money as a formless mass that you have, need, or both. In reality, your money is an asset made up of many components.

The more you understand all of the pieces involved, the better you’ll be able to manage your money. Organization makes that possible.

If you’re not certain how to organize your finances, start with these seven simple steps.

1. Set Payday Reminders

About 40% of American workers get paychecks every two weeks. But some people get paid monthly. Others get paid every week. Where do you fit into this spectrum?

Understand exactly when you're scheduled to get the money you're owed. And then dig deeper to determine when the funds will be available for you to spend.

Many companies use direct deposit methods to pay their workers. A third party accepts money from your boss, and that company transfers it to your bank. The transaction should be seamless, but it's not uncommon for a check to sit in your account as "pending," which means you can't spend it.

At Current, we deliver your paycheck up to two days faster with direct deposit if you have a Premium Account, as we credit your account as soon as we receive the information from the Federal Reserve. But if you're not banking with us and try to spend money that's not quite yours yet, you could get hit with a hefty fee.

And if you're paid via a traditional check, you could wait several days before the money hits your account. Banks need to chat with one another before funds are ready for you to spend.

Do this now to organize your income:

- Determine your technical paydays. Ask your human resources department to give you a list of all the paydays coming within the year.

- Talk with your bank. How long must you wait until you can spend your money? With Current, we credit your account as soon as we receive your direct deposit information, which is up to two days faster than traditional banks if you're a Premium Account member.

- Use your calendar. We'll be talking about calendars quite a bit in this article. Determine what tool will hold your important financial dates, whether you're using paper or an electronic version, and add in the dates when money will hit your account.

2. Identify Your Debts

It's easy to borrow money, and if you've done it often, you may have several different companies and individuals with claims to your finances. It's important for you to know how much you owe and when your payments are due.

You could have debt due to:

- Student loans.

- Car purchases.

- Payday loans.

- Credit cards.

- Mortgages.

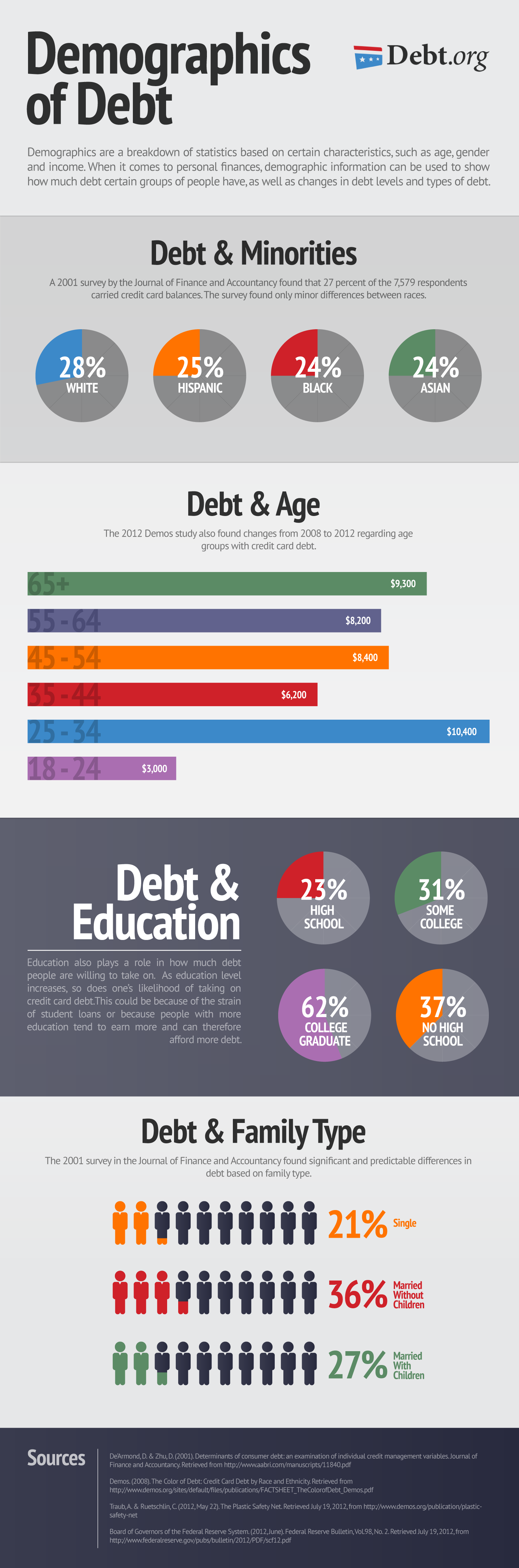

If you have debt, don't fret. Many Americans do. In fact, 23% of high school graduates and 62% of college graduates owe at least some money. But you can't pay back what you don't understand.

Do this now to organize your debt:

- Identify your creditors. Wade through your bank statements, credit card bills, and other assorted paperwork to determine who expects money from you.

- Understand your bills. Determine how much you owe on each account, and tally up the total to understand your full debt load.

- Use your calendar. Write down the due dates for each bill on your list.

3. Create a Billing System

About a quarter of all consumers like paper bills, as they think they're more secure than electronic versions. But many of us get a mixture of electronic and paper invoices each month.

Get control of your bills, so you're not overwhelmed with messages and uncertain of where to begin.

Do this now to organize your bills:

- Determine due dates for repeating bills. Look through your accounts, and make sure you understand when each one is due every month.

- Identify unusual bills. If you get some invoices (like HOA dues or tax prepayments) that only come occasionally, identify when they are commonly due.

- Use your calendar. Add all of the dates to your billing calendar, so you know when you're required to send money off to handle your bills.

4. Schedule Bill-Pay Dates

At this point, you'll know when money comes in and when bills are due. It's a perfect time to identify when you'll shift money from your account to handle your obligations.

You may find that tying bill-pay dates to your paycheck is wise. As soon as money comes in, it goes out again.

But you may discover that your bill due dates don't line up with your ability to pay them. You may be able to change your due dates with the companies you work with. Contact them, and tell them when you're typically paid. If they agree to shift your due dates, adjust your calendar accordingly. At Current, we deliver paychecks up to two days faster with direct deposits for our Premium Account members, which can help you pay all your bills on time.

Do this now to organize your bill-pay dates:

- Identify the right payment date. Determine when you'll settle in to handle your accounts.

- Bring the right people to the meeting. If you deal with your finances alone, you can pay bills the same way. But if you have a partner who is also involved in your finances, you'll want to pay bills together.

- Commit to keeping your appointment. Don't skip your bill-pay sessions. Make sure you're sticking to your resolution to pay on time.

5. File & Discard the Right Way

Whether you use paper or electronic versions, bills and statements generate a lot of data. To truly organize your finances, you must craft a plan for all of those bits and pieces.

A system can also help you ensure that you track both the bills you have paid and those you have yet to pay. Without it, things can get lost in the shuffle.

Do this now to create a filing system:

- Settle on a system. Will you accept only paper bills? Will you ask for digital versions? Or will you print the digital or scan the paper? Find a method that's right for you.

- Create a holding place. Anything you haven't paid yet should be in the same spot, so you can see it at a glance.

- Create an archive. Anything you've paid can slide into this folder.

- Clean up periodically. Walk through your archive and remove anything you no longer need. Formal documents, like ownership records or debt payment documents, should stay with you. But monthly bills could probably be discarded if you don't need them for your taxes.

6. Perform Monthly Budget Reviews

A budget is nothing more than a plan for your money. Create one, and you'll know how much you take in, how much you spend, and how much you save each month. But the best budget in the world won't help you if you don't adjust it.

Use tools in our Current app to understand your spending habits. How much do you shell out on things like coffee and snacks and gas? How much did you plan to spend on those things each month?

If you find that you're spending more than you thought you would, adjust your budget accordingly. Unrealistic goals can drain your willpower to even follow a budget. Make sure you're setting standards you can actually follow.

Do this now to organize your budget:

- Create a working budget. If you don't have one now, sit down and write notes about how much you make and how much you spend each month. Set goals for debt reduction and savings too.

- Track your progress. One day every month, look over what you had planned to spend and how much you spent.

- Assess your goals. Were mistakes inevitable due to circumstances outside of your control? Will next month be the same, or should you adjust?

7. Create Reasonable Savings Goals

If your plans involve spending everything you make, you'll never be prepared for the future. Look over your budget, and find ways to set aside money for both short-term and long-term financial goals.

You don't have to starve yourself or eliminate all of the fun from your life to develop a savings habit. It's perfectly acceptable to start with a very small goal and save just a few dollars per paycheck. But in time, and with organization, you can strengthen your resolve to save.

Do this now to organize your savings:

- Determine how much you've saved already. Do you have money set aside in a savings account? Do you have a retirement account?

- Investigate your options. Does your employer offer a pre-tax retirement savings account you can enroll in?

- Automate your savings. Use tools like our Savings Pods and round-ups to round up your purchases to the nearest dollar. You’ll save money with every transaction you make.

- Consider savings a bill. Set deadlines for shifting money into your savings accounts, and keep those commitments every month. Never think of savings as optional.

Let Current Help

Create a meaningful financial future with a little help from Current. We can help you understand how you spend now with insights on our homescreen and offers Savings Pods to make savings easier.

We also ensure that you get your money as quickly as possible with no hassle and no delays. We'd love to have you join us. Download our app and sign up in less than two minutes.

References

How Frequently Do Private Businesses Pay Workers? (May 2014). U.S. Bureau of Labor Statistics.

Demographics of Debt. Debt.org.

In Mail We Trust. (2015). Pitney Bowes.

Adjusting Your Bill Due Dates Can Help You Stay on Top of Your Bills and Manage Your Cash Flow. (November 2018). Consumer Financial Protection Bureau.

It's Hard to Stick to Budgeting and Saving Goals, but Easier if You Don't Rely on Sheer Willpower. ABC Life.

What to Do When Your Financial Goals Feel Unrealistic. Credit Counseling Society.

Current is a financial technology company, not a bank. Banking services provided by Choice Financial Group, Member FDIC.

Suggested Reading

{kind=link}